In 2024, B2B e-commerce in the US grew thirteen percent. Overall B2B sales grew half a percent. That is a twenty-six-to-one ratio. The organisations treating digital self-serve as an add-on channel rather than their primary growth engine are not just leaving money on the table. They are watching their most valuable buyers quietly migrate to competitors who built for how those buyers actually want to buy.

Digital Business · Business Infomatics Research Desk

There is a version of the B2B sales conversation that has been running for several years now about the changing buyer — the Millennial decision-maker, the self-directed research journey, the preference for digital interaction. It is a version that has been accurate but treated with a degree of strategic patience that is starting to look like a miscalculation. The data from 2024 and 2025 is not describing a gradual trend that will eventually require a response. It is describing a structural shift that is already playing out in revenue numbers, where the organisations that built digital-first B2B commerce infrastructure are growing at rates that are disconnecting them from the organisations still running primarily rep-assisted sales motions.

The global B2B e-commerce market was estimated at $32.11 trillion in 2025, according to Grand View Research — a figure that dwarfs B2C e-commerce by a factor of roughly five, and a figure that most B2C-dominated public narratives about the future of digital commerce have consistently underrepresented. The growth rate of that market is not distributed evenly. The organisations winning the largest share of B2B digital commerce spend are not the ones with the largest sales teams or the most sophisticated outbound programmes. They are the ones that built buying experiences that match how enterprise buyers want to purchase — and enterprise buyers, in 2026, increasingly want to purchase without a rep.

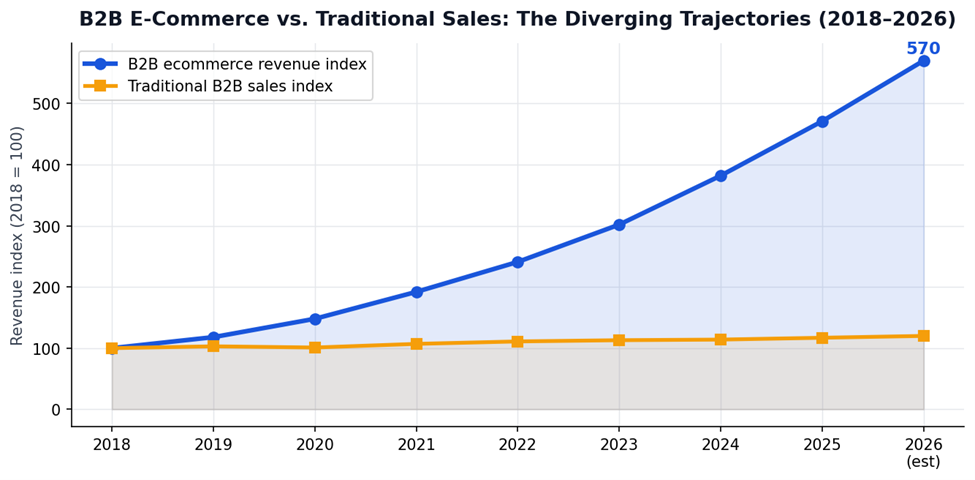

B2B e-commerce revenue index vs. traditional B2B sales, 2018–2026. The divergence has been consistent for seven years and is accelerating. Source: DigitalCommerce360, Grand View Research, 2025.

26× faster growth in B2B ecommerce than traditional B2B sales in 2024. In-person sales generated only 17% of B2B revenue last year, down 22% from two years prior. (DigitalCommerce360, 2025)

The B2B Buyer Who Doesn't Want to Talk to Your Rep

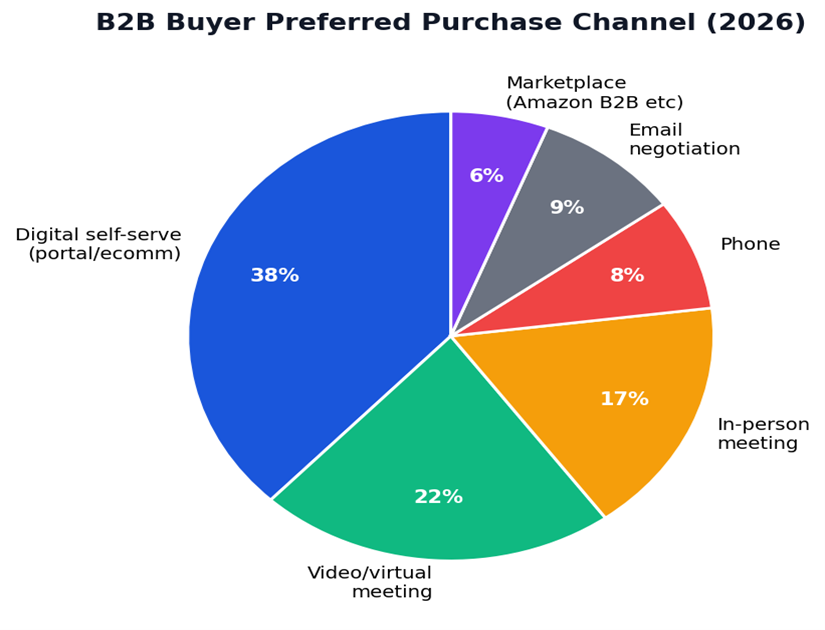

The research on B2B buyer channel preferences in 2026 is striking in its clarity. A McKinsey survey of enterprise B2B buyers found that more than two-thirds now prefer digital self-serve or remote interactions for at least the early stages of the purchase process. Thirty-eight percent cite digital self-serve portals or e-commerce environments as their preferred purchase channel — ahead of video meetings, in-person interactions, and every other option. Among buyers under 45, who now represent the majority of B2B purchase decision-makers, the preference for digital-first interaction is even more pronounced.

What is important to understand about this preference is that it is not primarily a preference for avoiding salespeople. It is a preference for control, speed, and the ability to evaluate options and make decisions on the buyer's own timeline without the process being managed by someone whose incentives are not fully aligned with the buyer's. When a buyer can access accurate product information, current pricing, contract terms, and reference data through a digital channel without waiting for a rep to prepare a proposal, that buyer can make a better-informed decision faster. The buyers who have had this experience with B2B vendors who have built it do not choose to go back to the rep-led process when an equivalent self-serve option is available.

B2B buyer preferred purchase channel, 2026. Digital self-serve leads for the first time, ahead of video and in-person. Source: McKinsey B2B Pulse Survey, 2025.

The Hybrid Sales Model That's Actually Winning

The framing of digital self-serve versus rep-assisted selling is misleading in an important way. It presents them as alternatives when the evidence strongly suggests they are complements — and that the organisations generating the highest B2B revenue per customer are the ones that offer both with intentional design about when each mode is appropriate in the customer journey.

McKinsey's B2B Pulse research found that buyers using ten or more channels in their purchase journey — a combination of digital research, content engagement, sales rep interaction, and digital purchase mechanisms — generate higher lifetime value than those using fewer channels. The insight is not that digital replaces human interaction. It is that human interaction is most valuable when it is deployed at the moments in the buyer journey where human judgment, relationship capability, or complex problem-solving genuinely adds value that the digital channel cannot — and that forcing buyers through human-gated processes at stages where they would prefer to self-serve is a friction cost that competitors who have removed it will consistently win on.

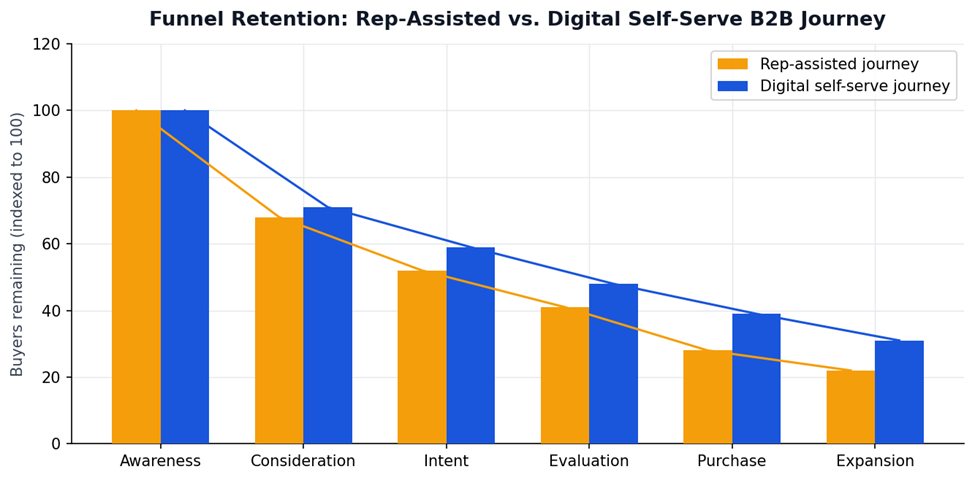

Funnel retention: rep-assisted vs. digital self-serve B2B journey. Self-serve buyers are lost at lower rates across every funnel stage. Source: Business Infomatics analysis, Forrester data 2025.

The Pricing and Configuration Problem Is the Technical Debt of B2B Commerce

The reason many B2B organisations have not built self-serve digital channels despite the clear buyer preference for them is not lack of strategic intent. It is the complexity of their pricing and product configuration. B2C e-commerce works with relatively simple product catalogues and fixed pricing. The typical enterprise B2B offering involves custom pricing by customer segment, volume discounts, contract terms that vary by relationship, product configurations that require technical specification, and approval workflows that span multiple internal functions. Building a digital channel that handles this complexity at a quality level that B2B buyers will actually prefer to a knowledgeable rep is a genuinely hard engineering and product problem.

The organisations that have solved it — industrial distributors like Grainger, software infrastructure providers, B2B SaaS companies with product-led growth motions — have typically invested in configure-price-quote (CPQ) infrastructure that sits behind their digital commerce front-end and handles the complexity of customer-specific pricing and product configuration without requiring human intervention for standard scenarios. That infrastructure investment is substantial. It is also, in the current market environment, among the highest-return technology investments available to a B2B organisation that has significant revenue locked behind a rep-required sales process.

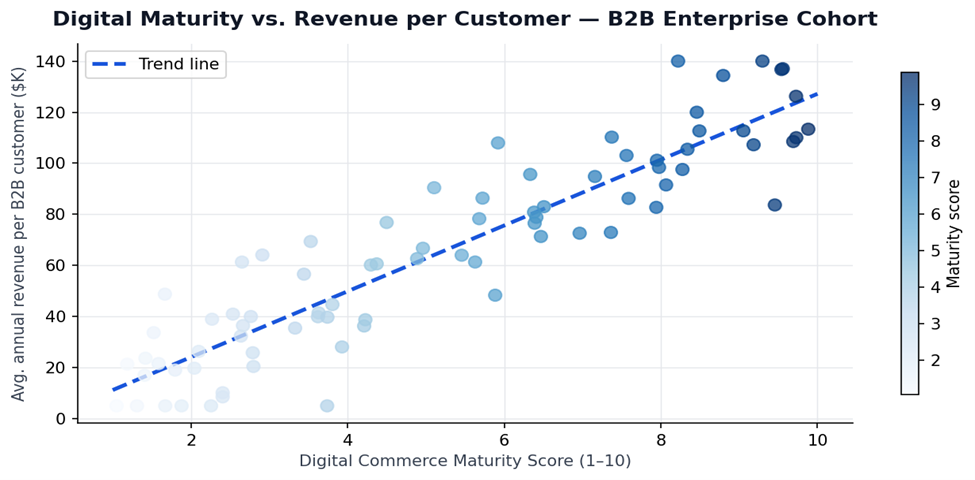

Digital commerce maturity vs. average annual revenue per B2B customer. The correlation is consistent and significant — higher digital maturity produces materially better revenue per relationship. Source: Business Infomatics analysis.

What Needs to Change and in What Order

For organisations that have recognised the structural shift in B2B buying behaviour and want to build toward a more digitally enabled commerce model, the sequencing of change matters as much as the destination. Attempting to launch a full digital self-serve commerce experience without the underlying data infrastructure — clean product catalogue, customer-specific pricing logic, inventory and availability data — will produce a buyer experience that is worse than the rep-led process it is intended to replace. The infrastructure investment is the prerequisite, not the parallel track.

The highest-return starting point for most organisations is identifying the segment of their product catalogue and customer base where self-serve is most feasible — typically repeat purchases of defined products at established pricing — and building a digital channel for that segment before attempting to extend digital commerce to complex configurations and custom pricing scenarios. The win from the first segment justifies the broader infrastructure investment and generates the internal data on buyer behaviour and conversion that informs the extension strategy. The organisations that tried to build the full vision at once have mostly produced expensive platforms that buyers don't use because the product and pricing data quality inside them does not meet the expectation the front-end creates.